Update on CBN's Currency Redesign

Things change, things stay the same

Some weeks ago, I wrote about the popular misconceptions (economics, not politics) around the CBN’s decision to redesign bank notes.

I focused mostly on what the policy can not achieve. If you have not read the article, it is linked below.

And the results are in, or at least some of it. Since the January 31, 2023 deadline has passed, we are starting to see data around the performance of the policy.

Please note that February 2023 data is not a perfect month to use considering that there was a one week extension of the January 31 deadline and the CBN decided to retain the old N200 note as legal tender on President Buhari’s request. Regardless, it helps us make sense of some aspects of the policy.

Let us look at some of the earlier narratives and compare with recent data releases.

#1 Currency Outside Banks (COB) Inconsistent with CBN’s Policy Position

Recall that the CBN interpreted having 85% or more of currency in circulation outside banks to mean hoarding.

“Significant hoarding of banknotes by members of the public, with statistics

showing that over 85 percent of currency in circulation are outside the

vaults of commercial banks.”

This week, the CBN released currency data for February 2023, the first full month of the implementation of the policy to phase out old notes.

In February 2023, currency outside banks was 85.9% of currency in circulation, basically at similar levels to October 2022 when the CBN announced the policy.

So, what now? Is it still hoarding? The CBN Governor continues to insist that it is bad, even during the MPC meeting this week. Even worse, he says that it affects the performance of the economy. I talked about this extensively in my first article and I have linked some parts of the commentary below.

#2 The Majority of Cash Outside Banks Returned as Deposits

Most people felt that most of the cash in circulation were with corrupt people and redesigning notes meant that they will be destroyed.

Looking at the data on currency in circulation and currency outside banks, we can clearly see that about N2.0tn made it back to the banking system. Currency in circulation fell by N2.3tn and the currency with banks reduced by N323bn, the net position is N2.0tn.

It’s tricky to account for the current N982bn in circulation to detect the full amount of the old notes that were returned as deposits.

What we know for sure is that:

Banks had about N138bn as at February (I suspect it is mostly old notes that were not legal tender), with N843bn outside banks

Notes that were not redesigned but in circulation stood at N145bn as at 2021

Old N200 notes that was reintroduced after the deadline was N245bn as at 2021

Around N300bn of newly redesigned notes had been introduced by mid February

Once you add 2-4 above, it means we can account for N645bn out of the N843bn currently outside banks. There might be overlaps with 1, but it is highly unlikely given that it is not sizeable and banks struggled to release cash to the public - it means they were mostly old notes that had been redesigned and not legal tender.

On this basis, I estimate that about 93% of the initial cash outside banks are now in the system.

With the recent extension of the deadline for the all the redesigned notes to remain legal tender until December 2023, one can expect that most of the cash originally in circulation will make it back into the banking system.

#3 Consumer Prices Continued to Rise with Inflation Reaching 21.9%

There were high expectations that the currency redesign will lead to a moderation in inflation but we are yet to see that.

Instead, inflation rose to 21.9% year-on-year in February 2023 from 21.8% in January 2023. Comparing consumer prices in February vs January strictly, inflation was 1.7% month-on-month, barely moderating from 1.9% in January 2023.

The expected impact of the currency redesign to lower inflation is nowhere to be found. I hinted at this when I said this in my earlier article:

To suggest that redesigning 6.6% of money supply - which is not going to be destroyed but converted to bank deposits (excluding those that don’t make it to the bank) to be later spent - is the solution to inflation is insane.

There have been different theories put forward to explain this. Some say the supply side nature of inflation is the reason, which is basically that money has no impact or a weak one on inflation.

Other say maybe output also reduced due to the cash crunch, basically meaning that there was not as much goods and services supplied for consumers to buy.

I do not believe both. I explained how inflation can fall in my prior article, the quote below is pulled from there.

Of course, if you take away bank notes in a country where a lot of people rely on cash to spend, it could slow down the rate of price increases in the very short-term. And that is if one further assumes that a significant share of transactions is done in cash and people are unable to switch to other means of payment. But that would make no sense because it would damage the economy.

My theory is that if cash penetration in the informal economy is high, there is no way a 70% decline in currency in the hands of the public would not affect demand significantly and put downward pressure on inflation. Unless people were able to switch to a large extent. So, yes, even though there was a great deal of pain, many people explored alternatives as they deposited money into the banking system. After all, we are sure most of the money in the hands of the public made it back.

Inflationary pressures were sustained because demand remained high as people found alternative means of spending in the absence of cash.

This is not to say other factors aren’t influencing inflation, but we cannot just ignore the 70% reduction in currency in circulation.

In fact, my next best theory is maybe the cash economy was exaggerated.

Unfortunately, normalcy resumes in March with the Supreme Court directive for old notes to remain legal tender, so we cannot analyse any other month like this.

What other theories are out there? Please let me know by commenting.

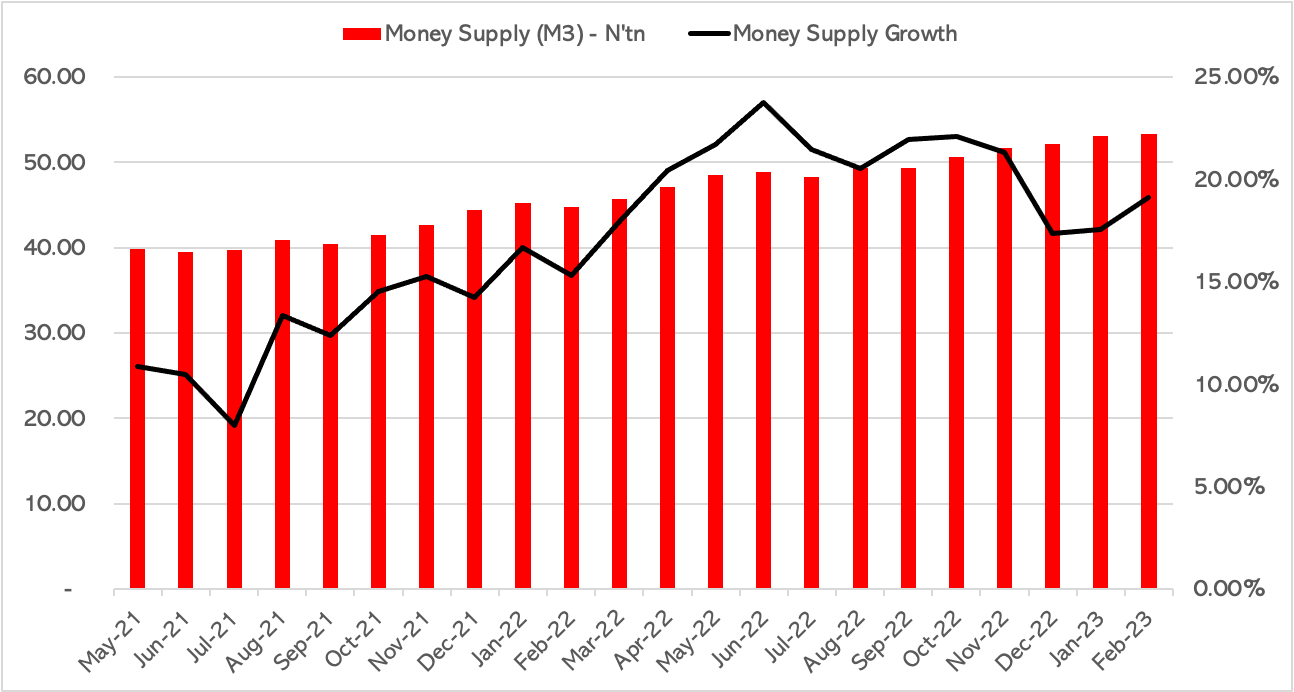

#4 Money Supply Continues to Rise at a Rapid Pace

In my earlier article, I mentioned that if we truly care about inflation and want to do something about it, what should be worrying is the pace of growth in money supply.

To curb inflation, one thing the CBN can do is to slow down the pace of growth in money supply given the long-term relationship between both. And unlike most people think, money supply is not just currency outside banks. It includes current account, savings account and other near cash (money market funds etc) balances. Currency outside banks, which the CBN was worried about, is only 6.6% of total money supply. Think about it — what do you spend when paying with bank transfers and debit cards?

Well, the results are in. Money supply expanded to N53.3tn in February 2023 from N50.6tn in October 2022 when the currency redesign was announced. The level of cash in circulation has fallen sharply, but not the amount of money in the economy. Remember, money is money, whether cash or demand deposits.

Between January 2022 and February 2023, the year on year growth in money supply averaged 19.8%. This is insane as it means over the long-term, if this persists, we can expect inflation to be around 20%. Some might argue that the relationship between money supply growth and inflation is weak but I’ll say it is weak not non-existent.

Ignore these tiring currency redesign debates, this is what is important and unless the CBN starts slowing the pace of its money supply growth to around 12% (in line with an inflation level that does not affect growth) or 9% (in line with its inflation target), we are in trouble.